Modern finance infrastructure for digital health

How new solutions enable digital health companies to work with insurance

Many digital health companies started as direct-to-consumer businesses. This approach simplified a lot on the payment side as Hims & Hers, Ro, and their peers did not have to deal with contracting and claims processing with health insurance. Currently, they are mostly taking cash payments from their customers. However, several trends exist that will encourage virtual health startups to become part of an insurance network and enter the "revenue cycle" world:

Billing insurance is a much larger market than cash pay, and people want to use their health benefits.

More complex procedures are more expensive and exceed many patients' disposable income, so cash pay is not really an option.

As digital-native patients grow older, they will require more complex treatments over the next few years.

Modern approaches to health care, such as remote patient monitoring and telehealth visits, are increasingly reimbursable with health plans.

Virtual health startups will need a modern finance stack to support insurance reimbursements, and the stack should simplify the billing process and integrate with other parts of their business. So after looking at technology enabling virtual health last time, this week, I will look at a modern finance stack for virtual health providers. Billing for digital health is not an easy process and involves several steps.

Revenue Cycle 101

First, let's have a quick overview of how getting reimbursed by a health plan works for providers. First of all, the provider has to get in-network with health plans. Once the provider and insurance have a contract, the provider can start submitting claims for fee-for-service models. Alternatively to fee-for-service billing, a provider might also want to join a value-based payment model.

Enrollment with a payer (become in-network & manage the relationship)

Becoming part of an insurance network is currently a pretty long and tedious process involving quite a bit of paperwork. The process can be separated into two stages: Credentialing and Contracting.

During credentialing, the provider has to meet the insurance's internal criteria set forth for the providers in their network. These credentials include state medical licenses, malpractice policies, and other documents. Gathering and verifying all these documents is particularly arduous for digital providers who want to serve several states. There are about 150 state-level boards that each has different requirements. On top of that, each health plan has its own slightly different criteria and verification processes that can take very long and involve a lot of back-and-forths. This process can take from 2-5 months for each insurance.

After the provider has been credentialed, the contracting can start. The insurance will extend a contract to the provider, including the reimbursement rates and other details and responsibilities for participation in the health plan's network. If the offered rates don't meet the expectations, there is also a negotiation phase. It depends on the size and location of the practice, how much negotiation power they have to adjust the rates. The contracting process can take another 45 days. There is no negotiation phase for participating in government programs, as Medicare/Medicaid sets the rates.

Once the contract is signed, the provider must further manage the contracts. This includes updating expired credentials, renegotiating rates regularly, and updating the contract in the billing system to file the claims correctly.

Fee-For-Service billing

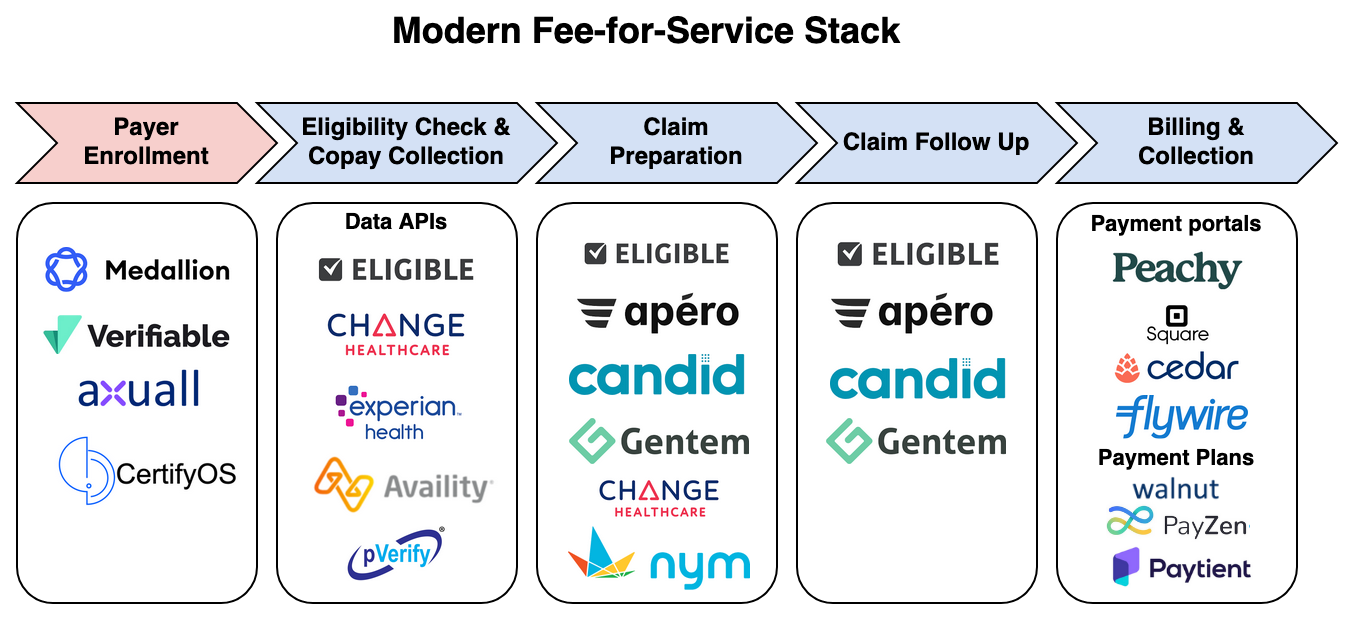

Fee-for-service billing is a well-established field, and there are a lot of legacy vendors providing billing and practice management software (more on that later). Let's have a quick overview of the main steps happening during the reimbursement process:

Patient Registration, Eligibility Check & Copay Collection: Before providing any service, the provider must verify that the patient is covered by insurance. All the media attention to surprise bills made consumers wary about understanding their coverage upfront. The practice will also need to determine whether the patient has a copay or has not met their deductible. In these cases, they will need to collect the payment from the patient. Also, the provider needs to make sure that all prior authorizations and referral requirements are met. For certain health plans, like an HMO, a patient first needs to get a referral from their primary care provider, before seeing a specialist. Also certain procedures and many specialty drugs require prior authorization - these strategies are set by the insurance companies to avoid overutilization.

Claim Preparation & Submission: After the service, the provider will need to prepare a claim for the health insurance. This involves translating the EHR documentation into treatment and diagnosis codes (CPT & ICD-10 Codes). Smaller practices usually outsource this to a billing company and hospitals have a large coding team that does this. After coding, the claim can be filled out and sent to the health insurance. Usually, the provider does not transmit the claim directly to the health insurance but routes it through a clearinghouse with connections to many insurers.

Claim Follow Up: After the claims have been processed, i.e., adjudicated, by the health plan, there can are a few outcomes worth diving into:

Claim accepted & paid: self-explanatory

Claim rejected: The claim has some details missing or is not filled out correctly, i.e. the member name is not spelled correctly or the date of service is missing.

More info required: The payer might request more information, documentation to be able to adjudicate the claim, for example lab results that show medical necessity, etc.

Claim denied: The health plan finds the claim not eligible for reimbursement. In certain cases the provider can appeal this decision and resubmit the claim.

Here is a good overview of the possible states a claim can be in.

Billing & Collection: These days, in most cases, insurance does not cover 100% of the procedure costs, so the remainder of the bill will need to be sent to the patient. Invoicing should be done online in a modern setting, and digital payment methods should be accepted. For larger bills, the provider might want to offer payment plans (without interest) or financing plans (with interest) to the patient. Collecting outstanding balances after the procedure is quite a pain point for many providers and intelligent reminders and reducing the friction for payments can increase the collected amount. For many practices the collection rate is quite high, but hospitals often struggle with collecting payments after the patient has left the hospital.

Joining a value-based payment model

While fee-for-service billing is a well-established process, value-based payment models are the wild west. Countless programs exist that all follow different approaches to share risk with the provider. They range from shared savings compared to historical cost benchmarks to fixed payments per patient or clinical episode. Some arrangements require the provider to join an ACO, and others can be done directly with the payer. Most have quality data reporting requirements. From my point of view, signing up to a value-based payment model seems very specific to each program, and there are no great processes established yet.

Several vendors have started to build the infrastructure to support these workflows

The growth of digital health providers has exposed how much of the processes are broken. While single practices probably have accepted the paperwork involved when dealing with insurance, digital health providers operate at a different scale. When they want to expand across states rapidly, these arcane processes are a significant blocker for scaling their business. However, many legacy technology vendors don't fulfill the requirements for a modern tech stack solution. They often don't follow an API-first architecture and don't have a lot of intelligence and automation capabilities. So early digital health providers opted for building their own technology stack.

As it's not efficient that every provider reinvents the wheel, several new players are now tackling the challenges related to insurance billing. API-first products now address many of the aforementioned functions, but there is probably room for more solutions. Let's look at a few companies emerging in the insurance reimbursement space.

Enrollment with Payers & Value-based care

Derek Lo started Medallion after a conversation with Ro's CEO, Zachariah Reitano. Reitano mentioned that the biggest challenge in growing their telehealth business was obtaining and managing licenses in multiple states. Medallion offers a platform to manage providers' licenses. It is now entering the credentialing space, making it easier for digital health players to become part of an insurance network. Other players in this space are Verifiable and CertifyOS. Axuall is taking a more integrated workforce approach and offers licensing and credentialing solutions. As licenses and credentials expire, providers have to take care of this workflow on an ongoing basis.

Patient Frontend: Registration & Billing & Payment Plans

For a first-class "user" experience, it makes sense to consolidate all patient interactions into one portal, including insurance card intake, invoicing, and payments. Any third-party vendor that touches patient data is subject to HIPAA privacy and security rules. For claims processing, this is very obvious, but protected data also includes patient appointments, medical bills, and potential payments. Therefore, when building their payment functionality, digital health companies must be careful to stay HIPAA compliant and sign a Business Associate Agreement (BAA) with their vendors. For example, Square offers to sign a BAA, but Stripe is currently not. To help with the payment piece, some vendors have emerged. Peachy is offering an integrated payment experience for providers to accept multiple forms of payments, send reminders and track their invoices. This is similar to what Cedar built. However, they are currently targeting only large hospital networks.

Buy-now-pay-later is also entering the medical field. This is especially useful for patients with high-deductible health plans, who must pay up to $4,000 before their insurance kicks in. Walnut offers payment plans for patients that providers can integrate into their payment portal.

Billing API provider - Eligibility Checks, Claims Processing & Follow Up

On the backend side, a whole new group of companies has started that is set to make the interaction with insurance companies more seamless. These API-first businesses are trying to help providers integrate parts or the whole revenue cycle process into their workflows. Eligible started in 2011 as an API to check members' enrollment with health plans and co-pay determination. They recently added billing features that allow a provider to submit and track claims with the insurer. Candid and Apero are companies recently started to provide billing APIs and make the reimbursement process as simple as possible for providers. Nym is trying to solve the coding problem by applying NLP/ machine learning to auto-code doctors’ notes. However, I’ve heard from my AI research friends that auto-coding is a really really hard task, as the data quality is quite bad. Gentem, another player in the field, provides an all-in-one platform for independent provider groups to take care of their insurance reimbursement with data-driven strategies and intelligent automation.

Another noteworthy solution is Change Healthcare, which has been around for a while. Still, through recent acquisitions like PokitDok and others, they have built an API solution that got quite some traction with digital health companies. It's a great example of a legacy vendor that has adapted to a more modern and open approach, and they can leverage their existing relationships and integrations with payers.

Value-Based Care Automation

As mentioned earlier, setting up a value based payment model is story of its own. The classic ACO approach exists, i.e., joining an accountable care organization such as Aledade or from BCBS to become part of the Medicare VBC program. However, there are many drawbacks to this approach for digital providers. A vendor helping companies to join the CMS direct contracting program is Pearl, but CMS has paused the program, so it is unclear how Pearl will respond to this break/ change of direct contracting. There are also providers such as Innovaccer, Arcadia and Health Catalyst that help providers with the reporting and analytics required for successful VBP models. It’s probably worth it’s dedicated article.

[Comment: If you are a provider thinking about adopting a VBP-model, please reach out, I would love to hear your experience!]

My take on the modern finance stack

I am very excited about the dynamic currently happening in digital health. We are at the beginning of a classic disruption cycle. While digital health companies are still a small part of health care, they are willing to adopt a new modern tech stack, enabling them to focus on better patient experience and high-quality care. Here are a few thoughts on this:

Openness is critical: It's exciting to see that many of these new solutions follow an API-first approach. This will allow providers and other builders to mix and match these services for their solutions. I think anyone going into the space should keep this in mind. There are enough "closed" solutions available through the legacy vendors.

Generalists vs. Specialists: It will be interesting to see how these new infrastructure solutions evolve. Health care is a very specialized field, and different specialties and provider types have different needs. For example, a psychiatry billing API might beat a generic billing API to leverage the domain data better for their claim preparation and denial management. As health care is such a vast space, there is probably quite some room for smaller specialized players next to the general solutions. We can observe this specialization with the long-tail of outpatient EMR providers that are often tailored to a specific specialty.

Integration problem: With all these new open solutions, a critical issue will be orchestrating these services into one coherent experience for patients, doctors, and admin staff. A lot of efficiencies can be lost through swivel-chairing. Most digital health companies have their own developer teams to do the plumbing. However, it remains to be seen whether this is a sustainable approach or whether some integration hubs will emerge, i.e., the EHR or a practice management system, that brings everything together.

Gaps: With all these services, some gaps are still to be filled. One gap I see is for value-based care providers and handling enrollment and management of these arrangements. If you know of any players, let me know. Also, if you see anything else I am missing, please reach out. Also, many of the players mentioned are at the very beginning of their journey, and we will probably see them expand their solution space. For example, Verifiable & Medallion taking on the contracting piece, billing APIs becoming smarter with machine learning & better automation modules, etc.

Health plan innovation: It's also worth looking at the implications of a modern finance stack for health care on health plans. If the friction is reduced for enrolling into a health plan and managing billing, this will open the door for new types of health plans. Health insurance in the US is a highly concentrated market, and red tape is a barrier to entry. If a new plan can easily plug into the other end of credentialing & billing APIs, it will be easier to start operations and onboard providers.

Will payers reimburse digital health?: It remains to be seen how the reimbursement structure for digital health will evolve. Two questions to think about here: First, will digital health providers be able to prove overall lower costs and increased health outcomes? For payers to consistently adopt new virtual/ digital health CPT codes, this will be key. Second, will digital health companies be able to get long-term sustainable rates? Health plans realize that virtual visits are more cost-effective than in-person visits and might put quite some price pressure on digital health companies.

Thanks to everyone who gave input on this article. Particular thanks to @sanghavineil, @jbhansen & @healthbjk for reviewing the article - it got so much better with your input.

I am planning to update this post on a regular basis to add new players to the graph. So, if you want me to include your company or know a vendor that is worth being mentioned just reach out to my on Twitter @jfschneidr