Network Builders

How provider "networks" are becoming ubiquitous

Huge shout-out to Hui Cheng, Joe Mercado, Karthik Bhaskara, and Morgan Blumberg for their thoughtful comments on this article - great editors are the soul of any great article. (I am not necessarily claiming this one is, but the editors at least are!)

Happy Price Transparency Month! Since July 1st, 2022, hospitals and health plans are required to publish their negotiated rates in machine-readable files on their websites. Payers and health systems have long well-guarded their networks and contracted rates and saw them as an essential competitive asset. They cannot protect it anymore. This is a massive win for increased competition and to bring to light some of the craziness of provider-payer contracts.

While increased price transparency is a huge step, procedure prices are only one part when evaluating how much an episode will cost with a specific provider. The other parts are utilization and quality. Even if a provider offers lower per-service rates, the provider might not be the best choice from a cost perspective. They might tend to order more labs and images per episode of care or opt for more expensive treatment options on average. Another factor is quality of care - if a procedure, test, or image must be redone because of poor quality, a lower price will not matter.

With prices being more in the open, network builders will need to focus more on these other metrics, which are much harder to measure. Not only price transparency but also other trends are driving organizations to invest more into their network analytics and building out provider networks. In this article, I will take a closer look at everything related to network building!

Who is building networks and why?

Network building has long been a major focus for payers - it is a significant lever for them to use their volume to negotiate cheaper rates with provider groups and thus lower their total spend on health care services. However, they are not the only ones anymore thinking of running provider analytics - here are some other examples:

Self-funded Employers: Self-funded employers decide to bear the health care cost for their employees and thus are financially incentivized to optimize the health care costs of their employees. An important priority for them is to avoid large cost outliers. These high-cost areas include cancer care, transplants, orthopedic & bariatric surgery, fertility care, and maternity care. A single complex case in any of these conditions can easily double their yearly health expenses. Thus, they have started carefully selecting the right provider partners for these conditions to avoid adverse outcomes and exploding costs. Direct primary care, care navigators, and virtual care companies selling to employers have a similar incentive here and evaluate specialty providers based on cost and quality. This is one of their main sales arguments.

Value-based care organizations: With ACO Reach and the move to more and more fully-capitated models, risk-bearing providers will need to think more and more like health plans. A costly MRI or colonoscopy now directly affects their bottom line. Thus these organizations are starting to build their provider analytics stack to identify high-value specialists. Actually, legacy risk-bearing provider groups (for example California primary care groups) have been developing their own high-value networks for decades.

Virtual & digital health companies: Good patient experience is critical for digital health to retain patients. But the scalable virtual care model often clashes with the highly localized in-person model. Virtual care companies need to find the right partners for in-person care, so they will be able to handle more acute and severe cases. Identifying the right providers at a national scale and building relationships that support seamless handovers between virtual and in-person care is quite a challenge.

Payviders & Neo-health plans: Narrow network design has been touted as a new great way to reduce overall health care costs. This narrow-network strategy is pursued by several Neo-health plans and emerging hospital-affiliated "Payvider" health plans. However, these plans must carefully balance their preferred narrow network with adequacy requirements. (more on this below)

Cash pay platforms: Some people think the solution to many of the problems of US health care comes through cash pay networks. Cut out the intermediaries, make prices transparent and let patients decide. These new platforms are also building provider networks willing to take cash for their services.

What does network building mean?

Building provider networks is easier said than done and involves several steps. Here is a quick overview of things that you will need to do to create a performing provider network:

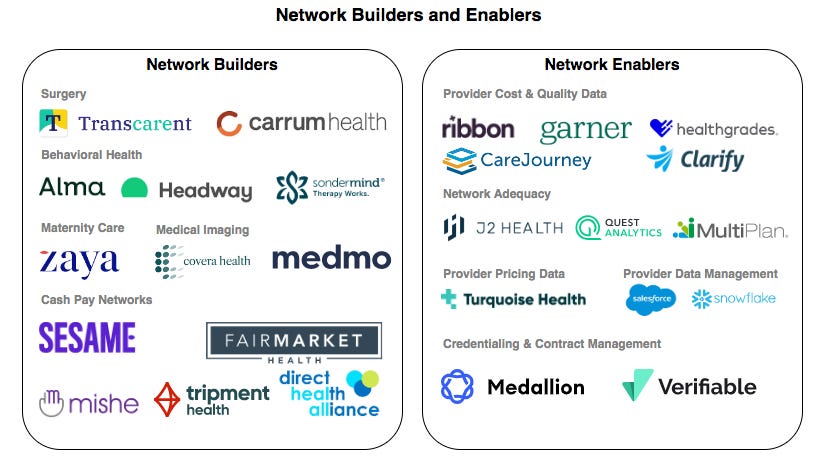

Adequacy: The first step for every provider network is to provide sufficient coverage for the health needs of its members/ patients. This means having enough cardiologists, interventional cardiologists, cardiac electrophysiologists and nuclear cardiologists etc. , that participate in the network. However, network adequacy is quite poorly defined. CMS has tightened its adequacy requirements for ACA, Medicare & Medicaid plans starting 2023 by adding more specialties to the adequacy criteria. One way to achieve basic adequacy is to borrow a network from an existing health plan, like Blue Cross Blue Shield or Aetna. There are also companies like Quest Analytics and (just recently founded) J2 Health that help organizations achieve adequacy and comply with regulations.

Refine your network for your need: After establishing basic adequacy, the organization will need to start refining its network. Several criteria can be taken into account: First, different populations have very different needs. For example, a health plan for construction workers will need much more orthopedic surgeons in their networks. A health plan focusing on Asian-American or Latinx populations might want more providers speaking their language and having cultural competencies. Second, there are other factors such as cost and the ominous "quality" factor. For many organizations, the network-building journey ends at this step - there are many consulting firms that help with one-off network optimization projects.

Collect Data on providers: More sophisticated organizations will start to build their own database around provider performance. There are several sources for doing this: 1) Claims data - this is often the richest internal data source a health plan/ employer or value-based care organization has access to. 2) External data vendors - companies such as Clarify, Ribbon, CareJourney, Turquoise, and Definitive Healthcare offer datasets on provider information ranging from simple things like address & phone numbers to more complex information such as episode quality metrics, cost metrics, and clinical specialization. Simple data points do not often mean easy: running my own analysis, I found that over 20% of the phone numbers in a payer’s provider directory are wrong - and this is probably a low estimate. 3) Organizations often also have access to several internal data sources, like patient surveys or even tribal knowledge from their providers, who often know pretty well which providers in the community one should work with and which ones to avoid.

Go out and build relationships with providers for contracts: Organizations might opt to create a one-sided network, meaning that providers don't know that they are part of the network and are selected to be preferred. However, in most cases, building networks means establishing a contractual relationship between the network organization and provider. These contracts could entail preferred rates, volume guarantees, or technology integrations. Establishing these contracts and relationships, in most cases, requires "boots on the ground" and can take quite a substantial amount of time to develop. For health plans, this contracting process is also called credentialing, and there are several companies in this space trying to make this easier.

Network enforcement: Once the network is established, the work is not done. To reap the benefit of the carefully constructed and negotiated network, one must also convince patients to choose the in-network network providers. This is easier said than done. Restricting network access through primary care providers didn't fly well with freedom-loving Americans when payers tried to establish restrictive Health Management Organization (HMO) plans. These days network enforcement has to be much more subtle and involves nudges, steering through assistance, and offering incentives.

Learning: Network building is not a static process - the world is constantly changing. The member needs are changing, provider's performance is changing. That's why network building is an ongoing activity.

Those are some of the basic building blocks for provider network building! Here is an overview of companies, helping with different parts of the stack!

Let's now have a look at some unique approaches to network building.

1) Networks addressing total cost of care

As already discussed, in the commercial insurance population, a few conditions make up the majority of health care spending. Most of the focus for payers and self-insured employers is to control these episodes' costs. One way of handling this is through bundled payment programs, i.e., shifting the risk for a specific condition to another organization and giving them incentives to properly manage their spending. Here are a few different flavors of these bundled payment networks:

Center of Excellence: This wonderfully sounding concept is not very well defined, but it often means that payers or employers partner with a select network of providers to care for specific, high-cost conditions. For example, Walmart partners with a dedicated network of clinics to take care of the following services: weight loss surgery, cancer care, hip replacements, cardiac surgery, organ transplants, and spinal surgery. As the biggest employer in the country, Walmart has enough volume to negotiate preferable rates and build its own preferred provider network for high-cost conditions.

Specialty-care networks: Center of excellence networks can also be "borrowed" from vendors aggregating these provider groups. If an employer does not want to go out and set up direct relationships, they have options. Many health plans offer center of excellence services with bundled payment rates. Companies such as Carrum or Transcarent's Bridge Health provide access to a network of high-quality providers and bundled payments.

Cash-pay networks: Cash payment networks are a newer trend in the same vein. The idea is to cut out the health plan intermediaries and create direct cash payment relationships between employers and providers. Instead of having a health plan negotiate rates with providers and resell them to employers, cash-pay networks usually let providers set their own prices for their episode bundles and act as a broker between employers and providers.

Specialty care navigators: Certain specialty conditions like cancer or musculoskeletal conditions (MSK) can be quite confusing for a patient, and making a "costly mistake" is easy. Specialty care navigators are helping patients to make the "right" decisions, understand their options, and allow them to access high-quality (and usually cheaper) provider groups. In many cases, they come with quite deep analytics on the quality and cost of their providers.

Imaging Networks: Medical images have high variability in cost and quality, and it is often a major focus for payers and employers to control their spending for these services. A few interesting companies in this space include Covera, which is building a network of high-quality imaging centers, and Medmo, which makes finding high-value imaging centers easier.

2) Networks filling unmet service gaps

Not every organization wants to build its own network. It takes time, lots of data analysis, and building contractual and integrations with provider organizations. So several organizations are building provider networks for other organizations to borrow, in particular in areas where access to care is often challenging and provider demand greatly exceeds their supply.

The line between network and health systems/ integrated practice groups is blurring here. Some of these network builders have quite loose relationships with their providers and act more like provider directories; others are fully integrated IPAs that come with a tech stack and unified branding. Here are a few examples for different focus groups:

Behavioral Health: Access to behavioral health providers has been notoriously tricky - due to stigma, the special relationship between patient and practitioner, and the lack of behavioral health specialists. Many digital health companies are trying to improve access to behavioral health. Examples here are Alma, Headway, and SonderMind.

Post-Partum Care: Similar to behavioral health, maternity care and in particular post-partum care have been challenging to find. Many health plans often don't have doulas and lactation consultants in their network, making it hard for patients to find providers and get these services reimbursed. Zaya Care is trying to change this by creating a network of maternity care providers that are in-network with several carriers.

Social Work: Social determinants of health are becoming more and more relevant and health equity got a much higher focus through the new ACO Reach program. Several vendors are making it easier for large organizations to connect with local social work initiatives. Unite Us is an example here, aggregating social work organizations across the country.

Culturally competent care: More and more health plans care care about serving historically underserved conditions and populations and they see providers with cultural competencies as a critical factors here. Companies such as Violet are training and certifying cultural competencies for providers and provider groups with a specific population focus are emerging, for example Zocalo for LatinX population and Rendr for Asian-American population.

3) Networks bridging virtual to physical

You can do only so much via video consults or asynchronous texting. Some exams and procedures just have to happen in person, especially for higher acuity patients.

I've spoken to several digital health startups, and many are thinking about how they should set up relationships with in-person providers. Digital care companies often want their in-person provider to follow a specific treatment protocol. For example, they often would like to establish new care protocols that allow their patients to move directly to procedure vs. having initial consult meetings.

Bridging virtual to in-person care is a nascent area, and I have not seen many players in this space yet, but I believe we will see more growth here. A great example is Solv health, helping digital care companies gain access to urgent care appointments. Their network of urgent care clinics can support many services needed by digital primary care. Another company in this space is Rezilient health, which is lending its in-person clinics to other digital care providers. This model is especially exciting as modern in-person clinics are probably much more flexible and innovative in supporting the specific needs of digital care companies than established health systems.

Thoughts

The fragmented nature of the US health care system with its thousands of payers and provider organizations makes network building an essential activity. Here are some further thoughts on this topic:

Provider networks offer a competitive edge: Even with price transparency rules making negotiated rates public and revealing some of the competitive advantages of provider networks and relationships, they will remain an essential competitive asset. A good understanding of utilization, quality, and negotiating preferred arrangements will still be critical for more and more health care organizations. It's interesting to look at which roles provider data companies will play in this new world. I believe that many provider data providers will become a commodity as they can be purchased by every provider organization, i.e., you have to buy them to stay competitive, but it won't provide you a competitive edge. Health care organizations must run analytics to gain an advantage and put their own spin on the data. A good analogy here is credit agencies - credit card companies have to buy your credit score but to really understand your creditworthiness and gain an edge over the competition, they will need to combine this information with their own data about you.

Network enforcement & engagement: Having had many conversations with value-based care organizations and employee-facing care solutions, I got the impression that many organizations are thinking very actively about provider analytics but don't invest a lot of resources into enforcing their network and nudging their members and patients to their preferred network. While it might seem a logical step first to find your targets and then think about how you hit the bullseye, it is also risky. All this investment into a preferred network might not pay off if you're unable to steer your members/ patients to the right providers. I find this problem so exciting that I will write another article about this topic.

Network contract market place: The complexity of provider networks will only increase in the next few years, and this will bring a whole set of new challenges. Insurance networks are pretty easy to understand, but a lot of organizations are starting to break the boundaries of these networks: they establish carveouts for certain conditions, they tier their networks, they develop direct-cash relationships with providers, etc., etc.! Many lawyers will have a blast billing their hours to establish and maintain all these agreements. I think there is a genuine opportunity to simplify network access for provider groups and reduce the friction contracting can take in the network building process. Maybe companies such as Medallion and Verifiable will enter this space. Their credentialing services greatly position them with provider groups to offer them more "networks and arrangements" they could join.

Network building is complex, and there is a lot of whitespace for products to be captured! Organizations are just starting to invest more resources into selecting their preferred network and analyzing how changing their network impacts their revenue and health outcomes.

If you're a healthcare organization thinking about network building & patient engagement - please reach out. I would love to talk!