Risk Adjustment - the new Revenue Cycle Management?

A short overview on risk adjustment and reporting

More and more health care organizations are ready to own their patient outcomes and are shifting from fee-for-service payment models to value-based payment models (VBP). But how much risk are risk-bearing providers actually willing to take on? A provider near a retirement home in Florida certainly has a very different population to serve than a provider in the East Village in New York (for non-New Yorker: East Village == young party people). Preconditions and other determinants of health are unequally distributed and therefore the patient outcomes are not always in the providers' control. Given this fact, should every provider get the same amount per patient per month, or should the provider with a sicker population get compensated more? This is where the world of risk adjustment starts. Risk adjustment is trying to compensate providers fairly for taking on patients with different risk characteristics. The rate per person is adjusted to their likelihood of incurring high costs.

As value-based payment models are on the rise and a favorite among many digital health startups, let's have a quick overview of how risk adjustment is applied in health care.

Market Failure in VBP: Adverse Selection

Risk adjustment is a fundamental mechanism for VBP models to work as a specific type of market failure would occur otherwise. Let’s assume we don’t apply any risk adjustment. If a provider does not want to make a loss, they would have to set their minimum acceptable capitation rate (= jargon for monthly rate they receive per member) at the average expected cost for both high-risk and low-risk patients. However, this minimum rate might be higher than low-risk patients are willing to pay and they (or their payer) might not want to enroll into a value based care agreement at these terms as they would prefer fee-for-service. Removing these members from the agreement will drive the average costs in the remaining patient pool higher, and even more healthier patients will not be willing to enter into a value based care agreement. This process repeats until only high-cost patients are left. [For the economists among my readers: this is an adoption of the adverse selection problem, called unbalanced risk pools.] Risk adjustment was born to address this classic market failure. It is a mechanism that tries to fairly compensate the risk-bearing entity for the expected costs of the patient given their preconditions and other health factors.

Risk Adjustment 101

To understand risk adjustment and its effects on health care, one should look at two different aspects. The first aspect is the actual risk model, which is used to calculate the risk scores for a particular member. Second, the provider or health plan has to report their risk scores once the risk model is calculated.

Creating a risk model

I am not an actuary, but in a nutshell, a risk model works as follows: First, find predictors for a patient's costs/ outcomes. Common predictors are demographic characteristics such as age, sex, income, Medicaid eligibility, and preexisting conditions like diabetes or asthma. Then all these factors will be put into a mathematical model (for example, a regression model), and the result of this model will be a risk factor for each patient's characteristics. This risk factor will determine how much additional cost a patient with this characteristic is expected to have. These factors can then be used in different use cases, such as to make contracts between value-based care providers and health plans or health plans and Medicare.

Risk factor reporting

After the risk model has been calculated (usually on historical data), the risk-bearing entity will have to report their actual risk scores, i.e., how many of their patients have diabetes, how old their patients are, etc. This sounds easy, but reporting risk factors can be pretty messy in practice. Data interchange is broken/ slow, certain ICD-10 codes are missing from the patients' records, or a patient submits claims for diabetes drugs but never got a diagnosis from their doctor during the reporting year. Also, because the risk score substantially contributes to a risk-bearing entity's revenue, there are incentives to be extra careful with reporting risk factors. Many organizations are conducting home visits to document missing diagnoses, and they are using data analytics to identify members with a so-called "risk gap" or "gap of care". I call this "risk reporting arbitrage", where risk-bearing entities exploit the fact that risk models are fixed, but the entity can influence the reported characteristics of their patients.

Use Cases for Risk Models in Health Care

Risk models are not only used for value-based payment agreements. Here is a (non-comprehensive) overview where risk models and risk adjustment mechanisms find application:

Capitation Agreements: This is probably what most people understand when talking about risk adjustment. Whenever an organization takes on the risks for the costs of a patient, their payment rate will be adjusted by different factors that make a patient potentially more costly. Like homeowners in hurricane zones, homeowners have to pay higher premiums than homeowners in areas with less weather risk. Risk adjustment factors (RAFs) can be found in value-based care agreements and Medicare Advantage Organizations, which assume the risk for their members.

ACA Health Insurance Exchange: The Affordable Care Act introduced two mechanisms to avoid the adverse selection problem in the health insurance marketplace. First, plans cannot refuse to enroll members and cannot charge different prices for people with preexisting conditions (except for a few exceptions like smoking). Second, a risk adjustment mechanism was implemented that transfers money from plans with many healthy members to plans with more unhealthy members. Accurately capturing reporting risk scores can often be the difference between a profitable and an unprofitable health plan.

Benchmarking Provider Performance Metrics (Costs, Quality): To measure a provider's performance in terms of quality and cost, one always has to consider their particular context. When confronted with high cost or bad outcome metrics, physicians often like to point out that their population is much sicker than the national average and that they can only do so much. Controlling for the patient’s risk, the cost and outcome metrics will be more telling.

Prediction models for interventions: The most immediate use of risk models is predicting a patient's risk (duh!). Risk models can help health plans or providers identify patients at risk for a costly outcomes. Health plans/ providers can direct resources such as health coaching or home health programs to that member to prevent these costs from occurring.

Thoughts on Risk Adjustment

Risk adjustment is an exciting space as it is the key to unlocking value-based care. Here are some of my thoughts:

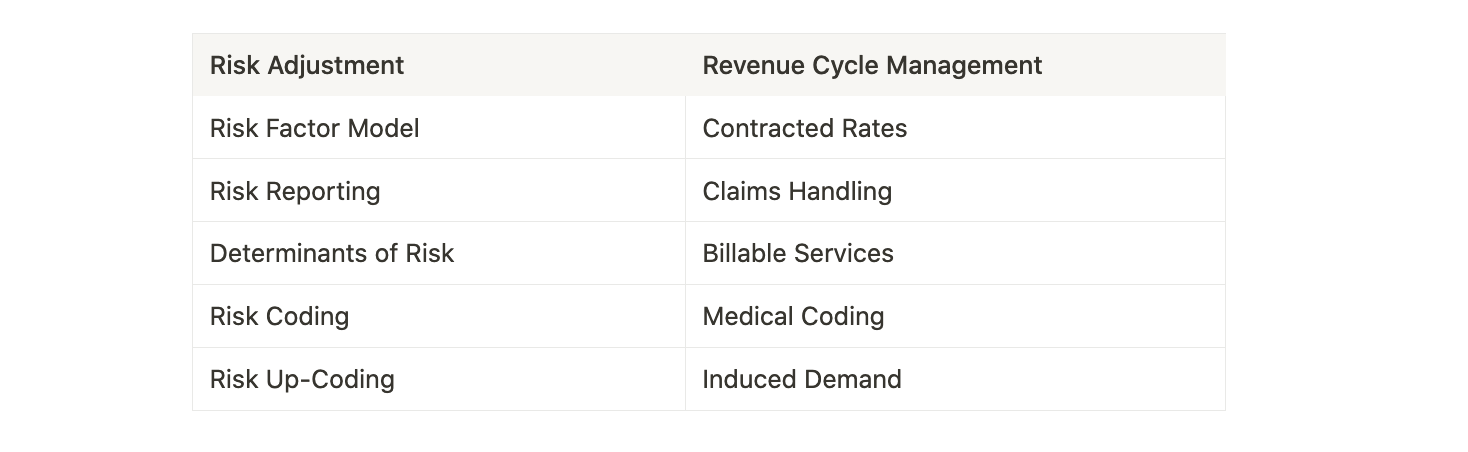

Risk adjustment departments are the new Revenue Cycle Manager: In a world where fee-for-service will be less critical, risk adjustment departments will play a more significant role in a health organization's profitability. I would think that the risk adjustment department at certain providers might soon become more critical than the billing & claims department. Here are some analogies:

VBP shifts incentives but does not do much about administrative overhead: As you can see from the table above, risk adjustment is quite some paperwork, especially if it coexists with fee-for-service billing. For example, the Medicare Shared Savings Program (MSSP) sits on top of fee-for-service billing, so there is now another layer of administrative burden on the ACO/ provider. I've written more about this here.

Digital health will need to find a way to properly "play the risk adjustment game": Getting risk reporting right is the same importance as fee-for-service providers setting up their coding & claims handling system. If they are not putting dedicated resources into this, they will see their claims denied/ risk factors not be accounted for, and they will lose revenue.

Risk management - a blessing or curse?: I have not made up my mind whether the emphasis on risk reporting is a net-positive or net-negative thing for society. The cynics might say frantic risk adjustment is just a form of up-coding, it is a zero-sum game, and patients are just getting "sicker" on paper but not receiving better care. However, we have to put the following things in the positive column: Without risk adjustments, the ACA marketplace would not work (because of the adverse selection market failure). Also, incentives for accurate risk reporting encourage providers to reach out to people with insufficient access to care.

Amazing post. I really appreciate your efforts.

https://cosentus.com/healthcare-revenue-cycle-management/

Great article! Thank you for writing! Any further thoughts in relation to MA plans massively overcharging? You're last paragraph was, unfortunately, prescient

https://www.nytimes.com/2022/10/08/upshot/medicare-advantage-fraud-allegations.html

Any positive news?