Why Health Care Needs More Capitalism

How closed-door deals are killing US health care - and how more competition can fix it!

When I am not writing, I am the CEO & Co-Founder of Arlo. We're on a mission to bring affordable health insurance to small businesses across the U.S.—and we need passionate, driven people to help us do it. We want to hear from you if you're excited about using cutting-edge technology to solve complex challenges! We're hiring Engineers & Sales professionals. Explore our open positions here!

We often take it for granted how amazing the free market is. But you realize it very quickly when you are in a situation where the market fails. This year, I went to Italy on a short vacation. We booked a rental car ahead of time, but our flight was delayed by a few hours. When we arrived at the car counter, the - not so friendly - attendant told us that our reservation had expired and we would neither get a car nor our money back. We were forced to book another car right on the spot for 4X the price of our initial reservation. The company truly exploited our situation, and because there was no alternative, we had to pay.

You probably had or know of someone who had similar stories with car rental agencies. It seems to be their business model to lure customers to their counter and then hit them with additional charges when people cannot price compare. They try to limit their exposure to a fair and transparent market.

Free and transparent markets are amazing - they allow you to trust that when you pay a certain price, you are getting the best value, and you can trust that you’re not taken advantage of. However, abuse of market power exists in many other industries other than car rentals. Probably the most critical is health care services in the US. Prices for health care vary significantly for the same services and are disconnected from the quality of care you’re getting. Today, I want to dive into some of the reasons why the free market is broken in health care and talk about some potential fixes.

{kind=link}

Why are prices so arbitrary in health care?

Let’s first talk about how prices for healthcare services are set! And I say prices - plural - for a reason, as there is no single price in health care. Every person pays something different when they show up at the doctor's office, even if they get the same services. There are two main mechanisms for how prices for healthcare services are set in the US:

Government Set Prices: A large portion of services are provided to people covered by traditional Medicare (not Medicare Advantage) and Medicaid programs. CMS and state agencies set the rates for each service by reviewing lots of data and consulting with different stakeholders. Providers who want to participate in these programs have to accept government-set rates. In other countries, this is the standard approach for all health care services, i.e., provider representatives, payer representatives, and government agencies get together every year to set a universal sustainable price.

Payer Negotiated Rates: Besides government-set prices, rates are usually the result of negotiations between payers and providers. This includes Medicare Advantage plans (privately administered Medicare) and health plans from the individual marketplace or employer-sponsored group health plans. While Medicare Advantage rates are often relatively similar to the CMS set rates, commercial rates vary wildly, sometimes up to 358% of Medicare rates. Rates also vary greatly between payers; some payers are able to negotiate better prices than others.

Provider-set prices: A final but very small number of prices are set by providers. These include cash-pay prices or the so-called charge-master rates, i.e., the official price lists that hospitals charge for care. However, these rates are usually never charged as most people either use their insurance.

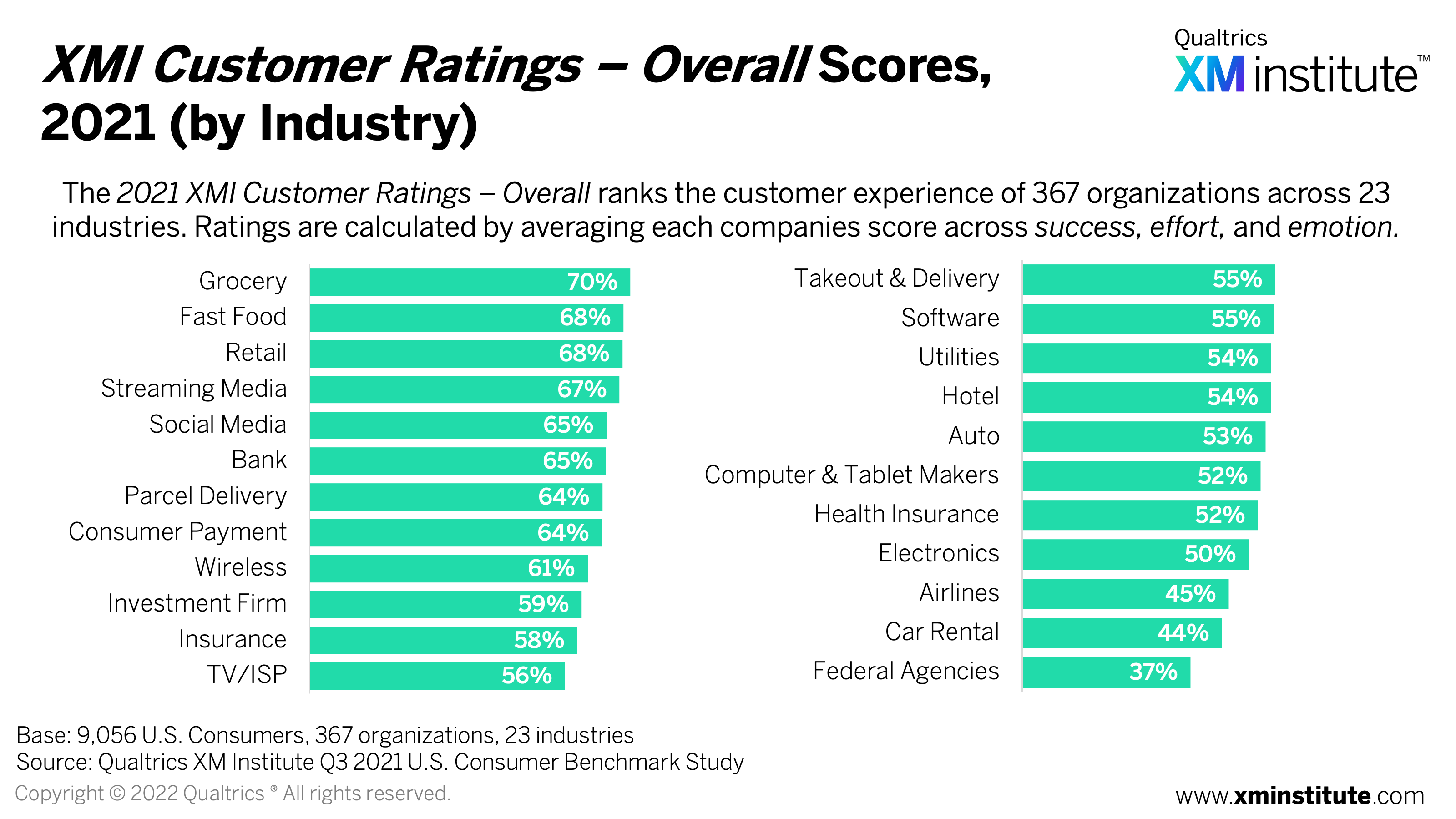

Free market proponents would argue that the government is not good at setting the right prices - they might have a point, but it seems like private companies are not doing any better. This graph shows an example of payer-negotiated hip-replacement rates in the Los Angeles Metro area, which are all over the place in terms of cost and not correlated to quality metrics. Note: If we had a functioning market, “provider-set” prices would be much more common - and market forces would punish or reward over-and-underpriced institutions.

Why Negotiations are broken

Let’s talk more about these payer-provider negotiations. Quality of care plays a role, but the hard factor in the negotiations is all about patients and payment volume. This is what represents negotiation power.

Thinking back to the car rental example, if someone can choose between different agencies, each agency will need to present itself with attractive prices or better services. But when there is only one agency around, they can charge whatever they want. Likewise, if there are many booking sites, car agencies will not list themselves on the most expensive platforms. But when there is only one booking site, the booking site can demand much higher referral fees from the rental agency. When it comes to rate negotiations, both payers and providers are doing their best to strengthen their bargaining power:

Payer consolidation: “UHC acquired Bind”, “Centene buys Wellcare”, and lately, “Cigna and Humana in Merger talks”. Payer M&A is ruling the headlines. There has been so much consolidation going on that we are now at the point where one or two health insurance players now dominate most markets in the US. In the large group market, for example, the average market share of the largest insurer is 63%, and the top three payers make up more than 80% in most markets. Payers are using this market power to negotiate preferred prices with healthcare systems. Because they control where patients can go through their network directory, they can push providers to give them lower rates. This is particularly true when providers don’t have much market power, i.e., smaller, independent clinics, which are what economists call price takers. These practices have to get used to the annual “rate update” letter by the large carriers. Payers also use price-setting power to create an economic moat. When they pay lower prices than their competition, they can offer lower premiums and gain more market share. Providers who are willing to give lower rates to larger carriers should bear in mind that they are making their counterparts’ negotiation power only stronger in the future.

Provider Consolidation: To keep their position at the negotiation table, providers developed other strategies to react. It is a common playbook for PE shops operating in health care: Buy a bunch of dermatology clinics in an area that used to be price takers from the insurance companies. Once you have bought enough providers in an area, they force the insurance company to the negotiation table to negotiate better rates and then sell the group with a profit. But this strategy is not just employed by private-equity firms but also by larger health systems. They employ highly paid M&A teams who have been buying out hospitals and practices, small and large, to ensure they become “too big to be out-of-network”. In 15 states, health systems are now the largest employer and, in many others, the second or third largest (behind Walmart).

Branding & Marketing: Another way to strengthen a health systems negotiation position and avoid being dropped from a payer’s network is to invest heavily in branding and marketing. This is to make sure there will be an outcry by insured members when a payer dares to remove a health system from their network. If you have ever driven on a Houston highway and wondered why not-for-profit organizations spend so much money on outdoor billboard advertisements or why they drop millions of dollars on Airport wallpapers, you now know why.

This dynamic between payers and providers has led to price competition drying up in many markets and is one of the reasons why healthcare prices behave so strangely. And we all pay for this in the form of rising costs in the form of…:

…Waste: When there is limited competition, there is no need to innovate, no need to become efficient - money will just come in, no matter what. This is why we still see antiquated technology in most health systems, bloated management organizations, and why most processes are still incredibly costly and manual.

…Payer Profits: Regulators decided to cap the profits that health insurance carriers are allowed to make by forcing them to pay out at minimum 80-85% of the premiums they collect. While this cap is probably well-intentioned, it creates a perverse incentive for payers - the main way health insurance can increase their absolute profits is not by reducing the cost of care but by increasing the total premiums they collect. So when payers negotiate with health systems, they might not negotiate as hard as they could, also because payers with market dominance know they can just push down the higher prices in the form of higher insurance premiums.

The lack of a free market is truly a root cause for many problems in the US health care system. But not all hope is lost…

Creating competition

Because health care costs are rising and somebody has to pay the bill eventually, more and more employers are looking for solutions to how they can maintain affordable benefits for their employees. Some employers and their third-party administrator partners are trying to break this unhealthy negotiation dynamic between large payers and behemoth health systems. Here is what they try to bring price setting away from the payer-provider backroom deals:

Reference-based pricing: The idea behind reference-based pricing is to tie a rate back to the state-set prices (which, in general, are deemed reasonable). Instead of negotiating rates, a health plan will pay up to a certain amount, and a provider can decide whether they accept the price or not. As this is a fairly uncommon way to get paid and reference-based pricing rates are usually lower than commercial rates, this approach creates some friction for members when accessing care. However, there are several health plans and vendors out there helping with setting up provider reimbursements and handling the friction.

Narrow networks & Direct Contracts: Some daredevil health plans are trying to break the “too big to be out-of-network” narrative and are trimming down their network to a few hand-picked providers. They find a set of providers they deem high-quality and then negotiate preferable rates with them. Providers sometimes are willing to agree to these rates as the plan will guarantee that they are the “exclusive” provider for their plans and other competing providers are not covered. This approach is very interesting. However, it requires that at least some competition is left in the market.

Procedure Carveouts: Certain high-cost procedures are highly profitable for many health systems. These procedures include cancer care, many types of surgery, as well as organ transplants. However, there are more and more facilities that specialize in this type of care, and that can offer these services at a dramatically lower price (and often better quality of care). Employers with enough power with large health systems sometimes carve out these services to certain specialty network providers to ensure their employees get the most cost-effective care for these conditions.

Dynamic Copays & Tiered Networks: Another way to increase competition is to align incentives between health plan members through different cost-share tiers. Instead of giving members carte blanche and the same copay for every provider, members will have to pay different copays depending on the provider they choose. Recent price transparency regulations have given rise to several vendors and plans that try to make costs transparent to the members. Unfortunately, many provider contracts prevent health plans from differentiating copays across providers within a health system or against other systems.

Cash Prices & Upfront Payments: Last but not least, some health plans are trying to leverage cash prices and upfront payments to obtain lower rates (and to avoid contract negotiations). The idea is that in some cases, providers may be willing to offer lower cash prices because they can collect the money upfront, thus having lower default rates and less billing overhead. Some health plans are built entirely around this approach; others have it as one feature of their plan.

Better infrastructure is needed

While many of the strategies above have been shown to reduce healthcare costs, there is still a long way to go to break the pattern of backroom deals between large payers and large providers and bring more competition to the healthcare market. However, operational challenges also need to be solved to make more competition possible.

Authorization Infrastructure

These days, when tapping our credit card, we don’t think twice. Neither does the merchant, as they trust the credit card system that once a payment is authorized, they will receive it. However, this has not always been the case. When the first credit cards emerged, the merchant had to call the card issuer to confirm whether the card number was still valid and if they could complete the transaction — an operational nightmare. So, back in the day, credit cards were only used for larger purchases, greatly limiting their use cases. Only when Visa and Mastercard built technology to automate transaction authorizations did credit cards start to displace cash. Doing authorizations and verifications via phone calls? Sounds familiar! Currently, most doctor offices are not set up to accept patients with “alternative access models” like reference-based pricing or direct contracts, even if they, in principle, would agree to the payment terms. From my experience at Arlo, I can confirm that practices may have a contract with a network, but because this network is not on the post-it note of the front desk attendant, they won’t accept the patient.

Health Care Service Marketplace

Negotiating narrow network contracts and direct contracts with providers is quite a feat. Fee schedules and side agreements can be very complicated and take time. Thus, providers are only willing to entertain contracting conversations when they think the number of patients is large enough. This makes it harder for smaller, innovative players to break in. The healthcare industry needs a standard contracting language that allows for easier network creation and payment for healthcare services.

Beyond Price Transparency - Network Freedom

I am a great fan of the recent regulations regarding price transparency in health care - however, they won’t achieve much unless we lift restrictions on putting this data into use. For example, many network contracts prevent health plans from adding copay differentials for different providers or allowing for network carveouts. For example, many health system contracts include inclusivity clauses, which means that a health plan’s network has to include all affiliated doctors. These clauses prevent employers from creating competition between providers and using quality and price data to steer members to the most cost-effective care.

Lets create more competition

Free markets are beautiful - they create vast value. The internet has created many new markets we never thought could exist: Uber for car sharing, Airbnb for spare rooms, and UpWork for international freelancing. We should work on bringing more competition to health care where providers compete to give the best care, and patients can be sure they are getting care worth their money. Feel free to reach out if you are building in the provider contracting or network space. Would love to have a conversation!

"For example, many network contracts prevent health plans from adding copay differentials for different providers or allowing for network carveouts. "

Don't think this is the best strategy from a member experience perspective. Healthcare is already confusing and copay differentials can add another layer of complexity to healthcare navigation.

Great post!