Bringing value-based to commercial health insurance

Launching Arlo - a value-based health plan

When I am not writing, I am the CEO & Co-Founder of Arlo. We're on a mission to bring affordable health insurance to small businesses across the U.S.—and we need passionate, driven people to help us do it. We want to hear from you if you're excited about using cutting-edge technology to solve complex challenges! We're hiring Engineers & Sales professionals. Explore our open positions here!

I’ve been excited about this post for a while now! Lately, I have been getting more and more questions about - Jan-Felix; what are you actually doing? You left Palantir now a while ago - what are you cooking up? It's time to open the curtains and give you a sneak peek into what we are building.

But before I get to that, I would like to share a bit more about what motivated me on this journey:

After undergrad, I got to experience the world of management consulting at McKinsey - a crucial part of their business is to help organizations streamline their processes and reduce unnecessary costs. I remember working on a study at an automobile manufacturer, where we sifted through every expense line to find opportunities to reduce costs. The manufacturer was struggling to keep up with their recent growth in business, and their unit economics were deep in the red. Nothing was safe, even the coffee machines on the factory floor (no worries - they kept them). We made sure that workers would practice on top of their license for example that line workers with higher hourly pay would not have to drive a forklift to get materials, but this task is done by forklift drivers who need less specialized training. We replaced parts from high-cost suppliers with lower-cost suppliers with similar quality. We reduced the inventory to free up capital,... - you get the gist. One thing I realized: In order to turn this company around, no silver bullet existed - not one initiative that turned a failing factory into a profitable business, but the aggregate of all the above yielded success.

Fast forward a few years, I got to work with some of the largest healthcare payers in the US. To me, they looked very similar to a poorly run factory - claims were not being paid-out to providers in time, millions of dollars in penalty interests were incurred, claims were adjudicated manually with inadequate accuracy, and there was no quality control when paying providers and facilities.

If a factory is poorly run, it will go out of business - and another better-run factory will take its place. Unfortunately, this dynamic does not exist in the US healthcare system. Poorly run payers found a way to make employers and patients pay higher and higher prices for their services, instead of having to improve their operations and increase their value. Read here if you want to know why.

And this is hurting people. I don't have to tell you about the devastating effects medical bills, high deductibles, and a lack of medical coverage bring to families across the country. 66% of bankruptcies are caused by medical debt, and many people are uninsured or underinsured because they don't think the premiums are affordable. We need a better way - something where payers are incentivized to create value. That's why we are building Arlo - a value-based health plan for small and medium-sized businesses.

Capitation in commercial insurance? How is that going to work?

While value-based care and capitated provider payments are prevalent in Medicare and Medicaid, they are still looking for adoption in the commercial space. There are several reasons for this:

The commercial insurance population is younger and healthier than the Medicare population. This means that, in general, a large quantity of healthcare costs is incurred by just a few high-cost claims, such as cancer, organ transplants, and premature babies. A lot of the playbooks from Medicare ACOs, such as better chronic disease management and home health for better access to primary care, have limited effects on commercial health care spent.

Health insurance coverage is tied to employers, and people change employers frequently. This means that health insurance carriers are not incentivized to invest in population health initiatives that only show effects after 1-2 years. They might not reap the benefits of investing in better preventative and primary care.

A lot of procedures in the commercial sector are profit centers for health systems. There is little incentive for them to cannibalize these profitable procedures through capitated payments - with the commercial rates often being a multiple of Medicare rates, this is a more significant issue than in the Medicare world.

While we are far away from the broad adoption of capitated provider payments in the commercial sector, we already have one form of capitated payments. We just call them differently: insurance premiums.

The role of health plans

At its core, the payer is the primary "risk-bearing" organization - it is their duty to offer access to high-quality care and ensure that premiums are spent wisely. By wisely, I don't mean that the health plan should decide on treatments and medical actions a member should take. That is and should stay the task of physicians. However, a good health plan should ensure that any money they pay out is maximizing the value for their members and the premium dollars are not being wasted on unnecessary care or unfairly-priced services. Together with a robust primary care team, the health plan should be the quarterback to ensure financially sound decisions are being made. A value-based health plan can achieve this without burdensome restrictions and unnecessary tedious utilization management. Instead, they should serve as a partner to the member and make transparent the financial consequences of their actions. The physician will decide on the course of treatment, and the health plan should open up different options for the member, explain their financial consequences, and make these options easily accessible. Here are a few examples:

Help members find out-patient facilities for IV-administered drugs, which often cost 3-5 times less than an inpatient hospital setting. Support them to easily get an appointment at these facilities and organize transportation.

Negotiate bundled payments for specific procedures and provide incentives to providers for high-quality outcomes.

Offer concierge care navigation to triage members to the right place of care and to avoid overutilization of specialists.

Make sure members have a primary care follow-up appointment after a hospital discharge.

... and 50 more things a health plan can do to reduce cost and improve outcomes.

Value-based health plans already exist. In fact, many large employer groups are running quite efficient value-focused health plans - their benefit levels are often much higher than small-group health plans. They employ data analytics teams, and medical management teams (for example, Morgan Stanley has their own Chief Medical Officer) and bring targeted population health solutions to their employees. Because these large groups are usually self-insured, they have the incentive to utilize their healthcare dollars most cost-effectively. It directly impacts their bottom line.

However, many people currently don't have access to these value-based health plans. Those are the small and medium-sized businesses in America. They either have to go with a community-rated health plan or are stuck with incumbent health insurance players, that even two years of work-from-home forgot that a lot of care could be delivered virtually, that have 60-minute customer service wait times, and that provider directories are as accurate as a phone book from 1998. These health plans often suffer from "vendor fatigue", which to me sounds very much like an excuse for not innovating and trying new approaches. Over the last decades, these health plans have not taken the necessary measures to offer better premiums: the most effective way to get better premiums was to reduce coverage by introducing high-deductible health plans and shifting costs from premiums to out-of-pocket cost sharing. It is time for this to change.

Announcing: Arlo - a value-based health plan for SMBs

I am excited to present Arlo - a value-based health plan for SMBs

We will keep a few details to our chest, but here are a few principles we are following with building out our plan:

1) Aligned incentives and performance bonuses

The key for a value-based health plan to work is to align incentives. Align incentives between the plan and the member, as well as the plan sponsor. The first element for us is to remove the perverse incentives of most fully-insured carriers by unbundling their services. When you utilize services from United Health Group, you most certainly have to use their owned PBM as well as stop-loss carrier and contract with UHG-owned providers. The ASO plan certainly doesn’t have the incentive to squeeze their owned entities for better prices or switch them out for a more competitive solution they don’t own. At Arlo, we don’t have these restrictions and are choosing the best-in-class vendors for our health plans.

Second, while most health plans are shared savings plans, fully-insured carriers are limited on how much they benefit from shared savings. Fully-insured carriers have to have a medical-loss ratio (MLR) of at least 85%, which means that 85% of the premium needs to go toward medical care. If a group has fewer expenses than that amount, the carrier needs to refund those premiums. This setup does not incentivize prudent financial behavior. For the health plan, it does not matter if a group has 60% or 70% in medical expenses. They will always make the same profit. Yes, they don't want a group to exceed 85% or even 100% - which would mean they will run a loss - but they usually address these high MLRs by increasing the renewal rates for this group or dropping them altogether.

Arlo is operating on a performance bonus with our groups. Our health plan will thrive if we can cost-effectively manage healthcare spending.

2) Unified Member Experience

Many employer-sponsored health plans suffer from a mesh of solutions that are bolted together rather poorly, leading to a disjointed member experience. While great care navigation solutions, convenient pharmacy apps, and good virtual urgent care tools exist, they must be optimized to work well together. I had to make this experience myself when I tried to access my care navigation app via my health plan portal and ran into an “App not found - 404” error. No wonder patient engagement is a challenge - nobody wants to juggle eight different apps to manage their health benefits. As the health plan, Arlo is in the prime spot to integrate different solutions into a coherent member experience. We built a modern digital member experience that integrates care navigation with virtual primary & urgent care. Our unified experience makes it easy for our members to make informed decisions about their care.

3) High-value providers & data-driven cost containment

I've written many of my thoughts on the opportunities for cost containment here, and most of them will find their way into Arlo in some form or another. I would like to highlight two elements here, though:

First, our health plan is built on identifying high-value providers and helping members find appointments with these providers. Prices and quality can vary a lot between providers, and we are using different data sources to identify the providers with high-quality that also offer a reasonable price. Our integrated care navigation team will then help members find the most appropriate and cost-effective care for their condition. We will write more about how we achieved this on our company blog - make sure you're signing up.

Second, we developed a robust, modern data infrastructure that lets us detect cost savings opportunities by monitoring claims, appointment bookings, prior authorizations, and member interactions with our plan. This intelligence layer ensures that nothing falls "through the cracks", and we identify cost savings opportunities in real-time.

4) Administrative Ease

To win with small businesses, you must make health plan administration as easy as possible. I was staggered when I learned in my conversations with HR leaders that many health plans only allow member enrollments manually via online forms without bulk uploads available. Imagine doing this every year for 200 employees...

Small business owners have a business to run, and it should not be their task to spend hours on bill reconciliations and payroll system syncs. Also, the HR teams at most companies already have enough to do with hiring, payroll administration, labor rule compliance, and DEI initiatives. They should not be their health plan's outsourced customer service department (which, in most companies, they actually are).

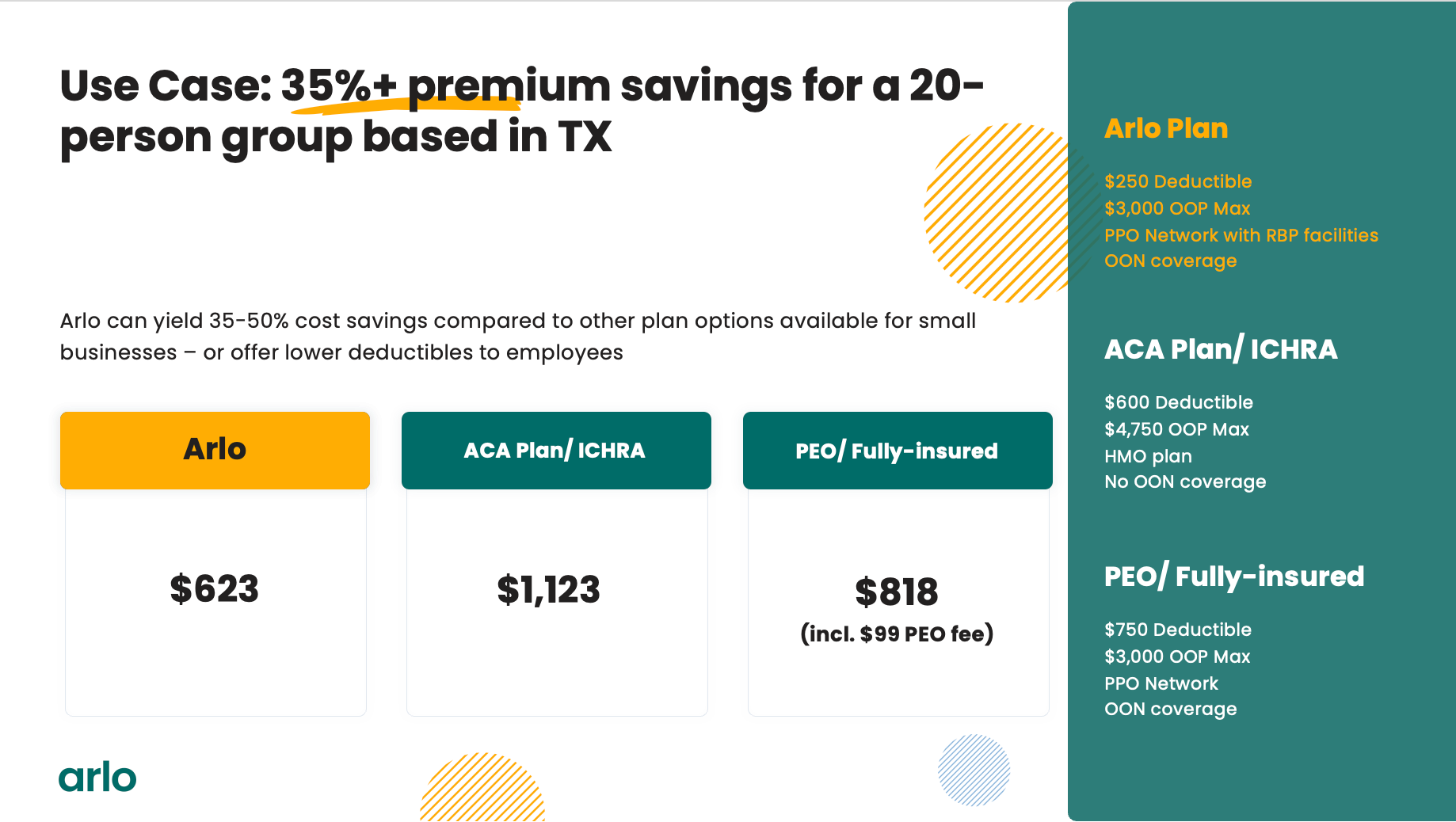

Aligned Incentives, a unified member experience, identifying high-value providers, and administrative ease are the four pillars of our plan, and I am very excited to announce that we are launching for enrollment in mid-year 2023. Check out the quotes we can offer compared to existing options for small businesses!

What this means for the blog

Building a health plan takes a lot of time, but I will continue publishing things and keep you with me on the journey - I will also start publishing more health plan-specific content on the Arlo website.

At this point, thank you all for being such great readers and supporting me on the way. I have met so many great people through these articles, including my awesome co-founder: Karthik Bhaskara. It's been a true pleasure working with you and building this company together.

I will share some more updates here moving forward - and if you want to continue to support me (and Arlo) in its mission to bring affordable health benefits to US workers, please share this post with a CFO at a small and medium-sized employer or with a broker you trust - I would love to talk. You can reach me at team@joinarlo.com. I am happy to show them around. And if you are an engineer or nurse/ care coordinator who wants to bring affordable health care to the US - we are hiring. Check out our open positions here.

Arlo is hiring - check out our job openings here.

Finally! Incredibly excited for Arlo to see the light of day and can’t wait to follow your journey 🚀

All the best Jan-Felix! Your blog has been real insightful and pleasure to read.